Insights

December 30, 2020

Reflation Nation

The year 2020 has been miserable — both in terms of human suffering and capital market carnage. Very few, if any, market prognosticators got this one right — and even if they forecasted a recession, it was for the wrong reasons. The pandemic meets Taleb’s criteria of a Black Swan event in that it was well outside the realm of regular expectations and had an extreme impact. As we (hopefully) bid adieu to the Black Swan of 2020, the seeds of recovery have been sown by monetary authorities, fiscal policy, and scientists globally. They have set the world on the path to recovery, but the policies unleashed may have investment implications for years to come.

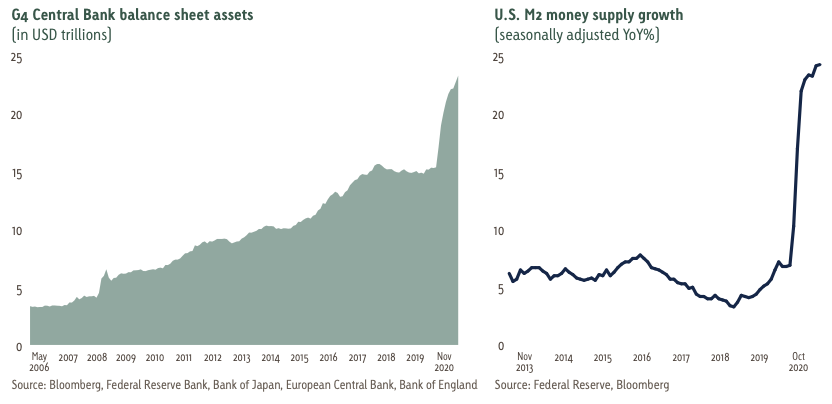

Central bankers have created huge amounts of global liquidity via Quantitative Easing [G4 graph]. In particular, the Fed has created an excess of U.S. Dollar liquidity, which further eases financial conditions for foreign countries [M2 graph]. In addition to this, fiscal stimulus from governments has been extremely generous, especially when compared to the amounts doled out in the wake of the financial crisis 12 years ago. [Federal stimulus graph] All this stimulus should continue to generate favorable conditions for risk assets globally.

It now appears that COVID-19 vaccinations will be distributed to front-line health care workers and the elderly in December 2020. With large swaths of the general population receiving vaccinations during 2Q21, we expect some level of herd immunity and return to normal economic activity by mid-year. The good news on this short vaccination timeline should give stocks the ability to look through the interim bad news of rising virus infections as winter comes to the northern hemisphere.

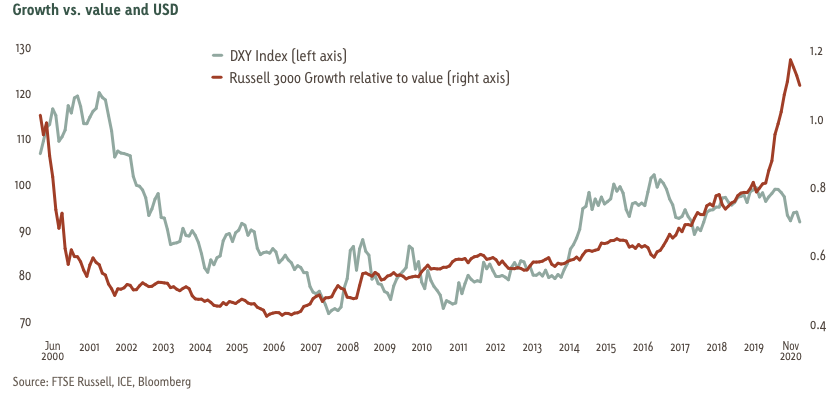

The early stages of economic recovery typically have a pro- cyclical bent with sectors such as industrials, materials, and financials outperforming. This dynamic may enable value stocks to outperform growth stocks during 2021 as a reflationary boom looms on the horizon, in sharp contrast to the last twelve years. If this scenario plays out, it has important implications for the flow of capital as the European, Japanese, and even emerging markets (EM) are weighted more heavily toward cyclical and value names. The U.S. stock market, with its emphasis on longer duration growth stocks, has benefited from the steep decline in interest rates. A reflation that steepens yield curves (central banks will keep the front end in check) could be another catalyst for shorter duration value to outperform growth. These capital movements, along with a few other dynamics, could also keep the U.S. Dollar under pressure as we move through 2021.

We believe that the Biden presidency will bring about a reversal of many of the Trump administration policies, which were positive for the U.S. Dollar. Trump’s protectionist policies were good for a self-contained economy like the United States to the detriment of those countries depending on free trade to sustain their economy. A Biden administration would presumably seek to repudiate at least some of those policies, moving more toward globalization rather than away from it. This, along with less confrontation and more predictability, would be positive for foreign currencies, which benefit from globalization and negative for USD.

We also believe that policies of the Biden presidency will lead to reflation and a weaker dollar. We expect more emphasis on fiscal policy to stimulate economic growth as monetary policy has just about exhausted itself. President-elect Joe Biden has already nominated former Fed Chair Janet Yellen to be his Treasury Secretary. Dr. Yellen is a pre-eminent labor economist by training and would presumably like to improve the fortunes of Labor in the Labor vs. Capital debate, as well as address some of the income inequalities that have plagued the United States. In Yellen’s November 30 tweet following her nomination, she might be foreshadowing the use of fiscal policy to address these conditions:

“We face great challenges as a country right now. To recover, we must restore the American dream—a society where each person can rise to their potential and dream even bigger for their children. As Treasury Secretary, I will work every day towards rebuilding that dream for all.”

www.cnbc.com/2020/11/30/biden-confirms-janet-yellen-as-nominee-for-treasury-secretary.html

Many on the far left of Mr. Biden’s political party advocate for Modern Monetary Theory (MMT), which holds that a country utilizing its own currency can spend freely since they can always print more money to pay off the debt. This faction also wants to use fiscal policy as a solution to address inequality and some of the social ills that have plagued the United States. It remains to be seen how far down this path we will go, but it is probably a safe assumption that there will likely be more debt-financed government spending with this administration. Even if the Republicans hold onto the senate, it is our belief that both parties have given up any pretense of fiscal responsibility and we anticipate inflationary policies that will further contribute to the dollar’s debasement.

A weak dollar would further enhance the pro-cyclical trade. As shown in the chart below, value tends to outperform growth as the dollar weakens:

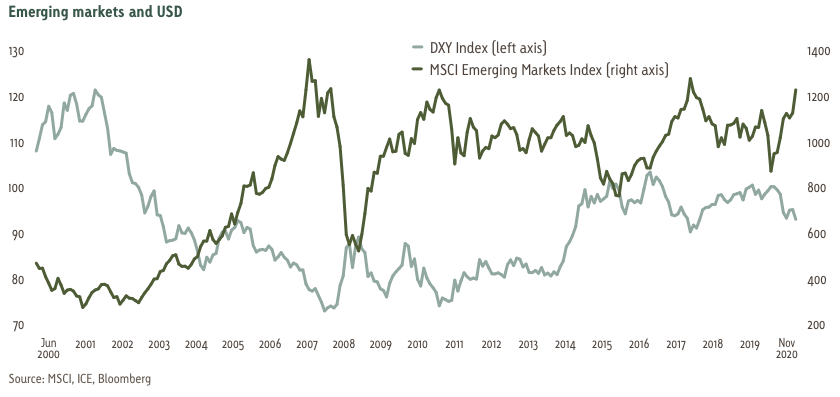

EM equity markets also tend to rise as USD weakens:

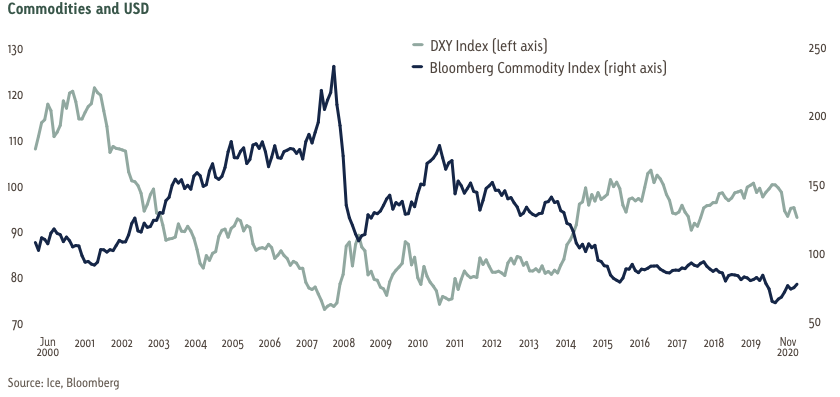

And finally, a weaker dollar could mean the beginning of a new bull market for commodities:

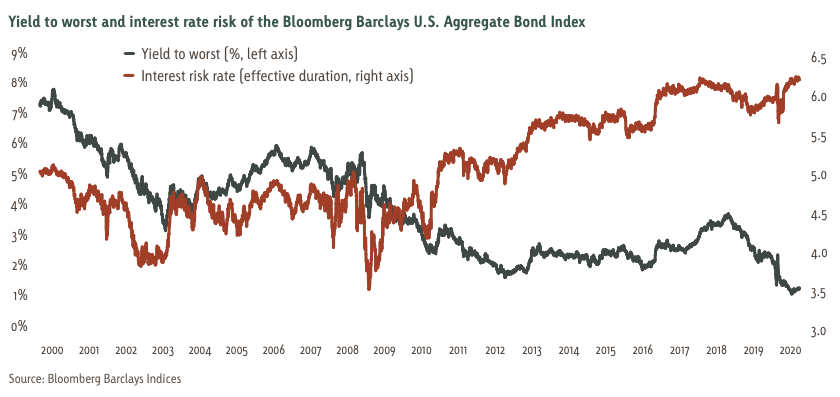

The potential inflation that accompanies these policies would be negative for bonds. To be clear, we are not immediately calling for 1970s-like inflation. We would argue, however, that the bond market is not currently priced for any uptick in inflation. Interest rate risk of the domestic investment grade bond market is as great as it has been over the past 20 years, while yields are close to 20-year lows, leaving little or no margin for error.

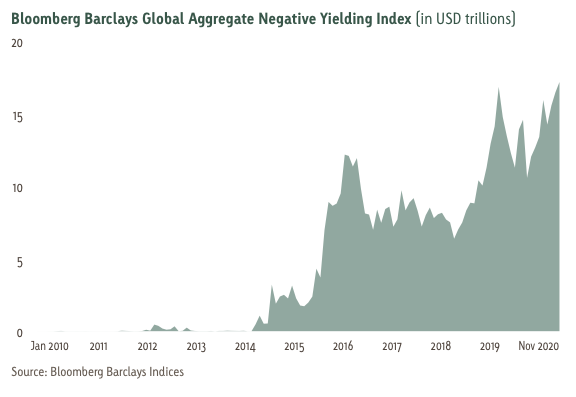

Digging deeper, we see that the U.S. 10-Year Treasury real yield is firmly entrenched in negative territory. Looking globally, we find $17 trillion of negative yielding debt — approximately 25% of the Bloomberg Barclays Global Aggregate Index.

In short, bonds could face a difficult period as reflation takes root and some of these economic policies are put into place. There are, however, some pockets of value in the bond market worth owning. Some of these examples include COVID-related casualties such as hotels, airlines, and energy. Caution is warranted, however, as some, but not all, will survive.

Commercial mortgage-backed securities could also perform well as some issues look attractively priced relative to the risk that workers do not return to the office. With inflation currently running low in much of the EM world there are some attractive real yields available. Owning them in their local currency can also provide some added return if their currency appreciates relative to USD. Finally, preferred securities are expected to offer value if the Biden administration keeps tough bank regulations in place — making preferreds the sweet spot of the capital structure for bank investors.

The pandemic has resulted in a world awash in liquidity and a tremendous amount of fiscal stimulus. As the calendar turns into 2021, we believe these aggressive fiscal and monetary policies, along with a healthy banking system, will be an important inflection point for investment professionals. We might find out if the Bond Vigilantes still have a pulse, and 2021 will be the year we start focusing on Real Returns again.

Conclusions and Observations

We advise being long global reflation and short COVID as governments and monetary authorities look to super-charge their economies and solve for COVID-19. With this as our thesis, these are our views:

- Favor risk assets over risk-free assets

- Favor equities over fixed income

- Value over growth

- EM and DM ex-US over domestic equities

- Favor inflation protected fixed income over nominal fixed income positions

- Long commodities and short USD

- Favor EM FX versus USD

- Long local currency EM sovereign debt

- Keep duration short of benchmark

As our parting comment, we would offer one optimistic thought going forward: The Spanish Flu pandemic of 1918 was followed by the Roaring Twenties, where the Dow rose six-fold from August 1921 to September of 1929.

Index Definitions

The Russell 3000 Index is a market-capitalization-weighted equity index maintained by the FTSE Russell that provides exposure to the entire U.S. stock market. The index tracks the performance of the 3,000 largest U.S.-traded stocks which represent about 98% of all U.S. incorporated equity securities.

The U.S. Dollar Index is used to measure the value of the U.S. dollar against a basket of six world currencies. The basket of currencies includes the Euro, Swiss Franc, Japanese Yen, Canadian Dollar, British Pound and Swedish Krona.

The MSCI Emerging Markets Index is used to measure equity market performance in global emerging markets.

The Bloomberg Commodity Index is a broadly diversified commodity price index that tracks prices of future contracts on physical commodities on the commodity markets.

The Bloomberg Barclays Global Aggregate Negative Yielding Index represents the negative yielding segment of the global investment grade debt from twenty-four local currency markets. This index includes treasury, government-related, corporate and securitized fixed-rate bonds from developed and emerging market issuers.

Disclosures

Red Cedar Investment Management, LLC (Red Cedar) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. Although taken from reliable sources, Red Cedar cannot guarantee the accuracy of the information received from third parties.

The mention of specific securities and sectors illustrates the application of our investment approach only and is not to be considered a recommendation by Red Cedar. The specific securities and sectors identified and described above do not represent all of the securities purchased and sold by Red Cedar, and it should not be assumed that investment in these securities or sectors were or will be profitable.

The opinions expressed herein are those of Red Cedar and may not actually come to pass. This information is current as of the date of this material and is subject to change at any time, based on market and other conditions. Past performance is no guarantee of future results.

An index is a portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance of certain asset classes. Indexes are unmanaged portfolios and investors cannot invest directly in an index. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.