Insights

January 09, 2023

Everything Old is New Again

Many things over the course of our careers have been declared dead, only to miraculously come back to life just when the masses thought the final nail was being driven into the coffin. After two decades of dreadful results, Business Week asked whether equity investing was dead in a famous 1979 magazine cover story.

In subsequent years, investors, journalists, pundits, commentators, and politicians have either questioned the existence or declared the following dead: inflation, bond vigilantes, active investing, value investing, U.S. hegemony, U.S. dollar (USD) strength, and the 60/40 portfolio. Some of these items, like inflation, miraculously came back to life and made a grand re-entrance by quoting the 1975 film Monty Python and the Holy Grail in declaring: “I’m not dead yet!” As it turns out, the erstwhile bane of all central bankers’ existence was simply on sabbatical as it came back with a vengeance in 2022.

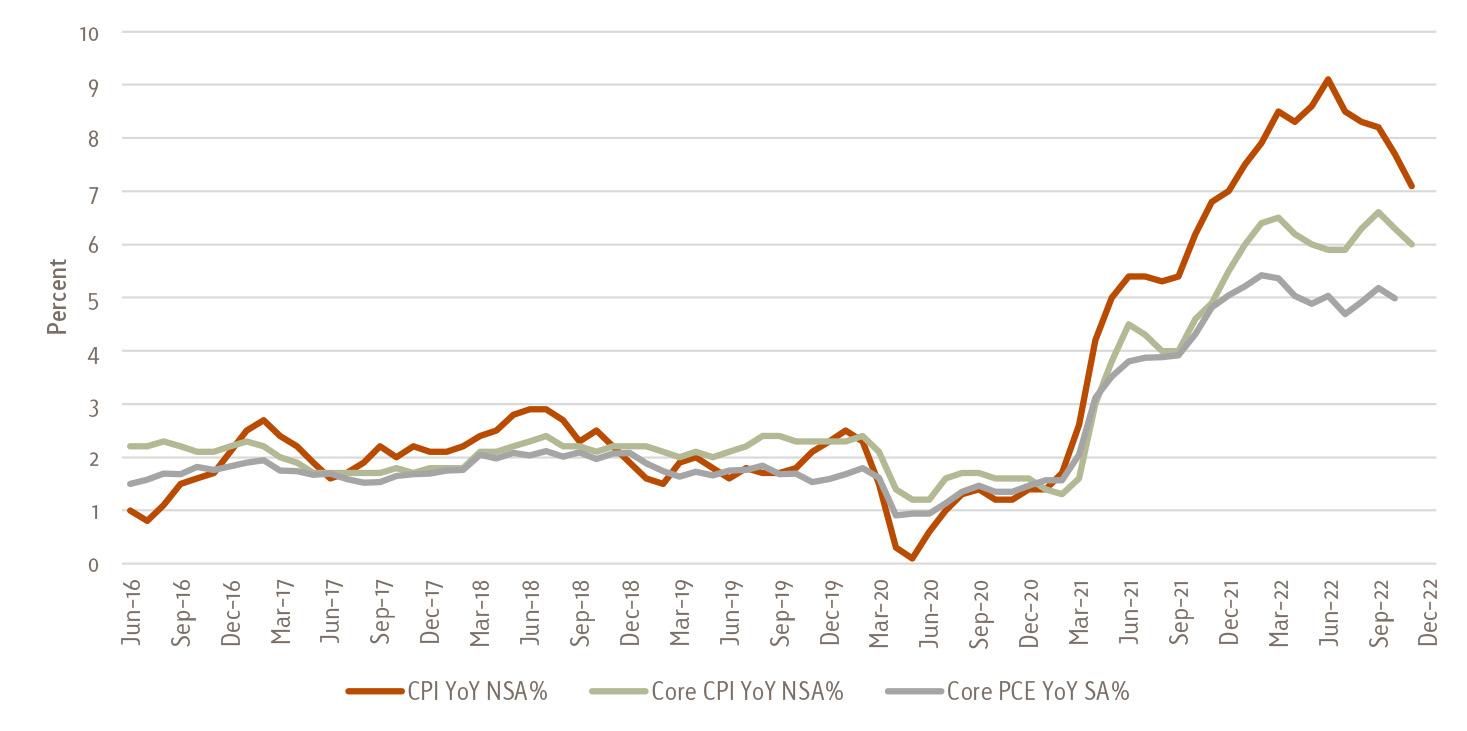

U.S. Inflation

Source: Bureau of Labor Statistics, Bloomberg

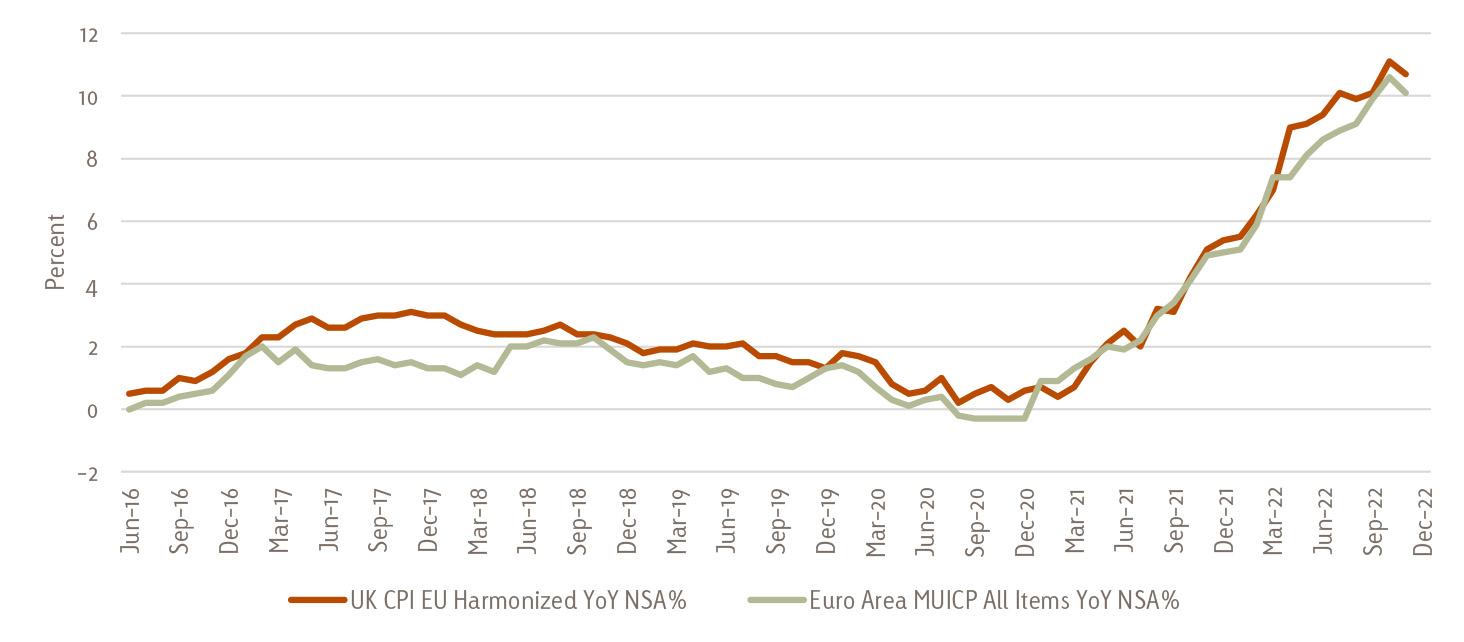

Source: Bureau of Labor Statistics, BloombergBy mid-year the headline number was reading 9.1% YoY versus the Federal Reserve’s (Fed’s) target of 2.0%. Meanwhile, across the Atlantic, the Europeans were grappling with double-digit inflation, with much of it energy related.

European Inflation

Source: UK Office of National Statistics, Eurostat, Bloomberg

Source: UK Office of National Statistics, Eurostat, BloombergFor the past 20 to 30 years, “normal” investing has meant allocating to a balanced portfolio of 60% stocks and 40% bonds or the so-called 60/40 portfolio. The idea was that equities would deliver performance over a long time horizon and bonds would be that rock in times of market volatility and equity market sell-offs. This rather benign investment environment came about through globalization. Developed countries began to outsource their manufacturing to China, with its seemingly limitless supply of cheap labor. As China exported disinflation to the world, markets and central bankers became extremely comfortable with the notion that inflation would become extinct (or at least go into hibernation). And indeed, they were correct for a few decades, getting to the point where the central bankers themselves and the capital markets could afford to be dismissive of inflation. They were so complacent, in fact, that the Fed and other central banks could afford to bend their core mandates of low unemployment and a 2% rate of inflation. They could virtually ignore the price stability goal since globalization would keep that in check. Being freed up from this pesky task, central banks could now afford to bail out investors from their speculative excesses. They could provide liquidity whenever the capital markets demanded it. They could backstop risky assets when global pandemics hit. These central bankers even found that they could maintain a zero interest rate policy (ZIRP) and in some cases a negative interest rate policy (NIRP). And in a complete departure from prior monetary policy, they found they were not limited to simply setting the short-term overnight interest rate. Now they could control both short and long term rates by purchasing government bonds across the term structure. The Bank of Japan (BOJ) and other central banks implemented yield curve control, while the United States opted for a softer touch with such things as “Operation Twist.” Emboldened by these new monetary policy tools, the BOJ even started purchasing equities. According to Richard Cookson of Bloomberg News, the BOJ now owns about $430 billion of Japanese stocks or roughly 12% of the NIKKEI Index according to our calculations. Its total balance sheet is 135% of gross domestic product per Cookson. According to its 3Q22 report, the Swiss National Bank holds 25% of its foreign currency reserves in equities. For its part, the Fed purchased both investment grade and high yield corporate bonds during the pandemic. In short, it was everything that capitalism was not—unaccountable, unelected bureaucrats were determining the price of money and, by extension, how capital and assets were being allocated across global markets.

From the investor’s standpoint, however, the playbook was simple: Own risky assets, and the more, the better. This meant equities and alternative investments such as private equity and venture capital. And use leverage if possible, the more the better. Afterall, the cost of capital was virtually zero and this environment would support even higher prices for risky assets. During this period, many investors embraced passive investing as active investing had seemingly passed on to the afterlife. If it did not matter which stocks you owned, why pay higher fees for active management? Another factor supporting higher asset prices was the presence of the Fed Put. If the Fed and other central bankers could be counted upon to bail out markets in times of turmoil, volatility could remain suppressed. Investors would not be willing to bid up the level of implied volatility in an effort to protect the downside to the portfolio if they knew the Fed had their back. Afterall, they owned the cheapest put option available courtesy of the Fed. The result of this has been artificially low levels of implied volatility in recent times—another factor that supported even higher asset prices. As we pointed out last year, we at Red Cedar believe the Fed Put is DEAD since they must now return to fighting inflation. With it, we also see the demise of ZIRP and NIRP. Without the Fed’s safety nets, risky assets have now begun the process of repricing to reflect the more symmetrical risk and volatility profiles of a bygone era. James Aitken of Aitken Advisors LLP refers to this as the era of “Everyone gets a trophy investing.” In the category of everything old is new again, we see a return to active management providing excess returns. We also believe value investing will continue to re-assert itself after it had been largely missing in action for the past decade. All of a sudden, valuation metrics are meaningful again when not masked by the dopamine of free money and big ideas. Growth stocks could continue to underperform their value counterparts as higher inflation, higher interest rates, and lofty valuations could impact their performance. Stock-pickers who had retired to the Villages in Florida after their near-death experience will feel rejuvenated as investors seek active management for their equity portfolios once again.

With 2022 being the worst year ever for bond investors, and the fact that it occurred during an ugly bear market for equities, many might be tempted to declare the 60/40 portfolio construction dead. We tend to disagree with this notion, thanks in large part to the return of bond vigilantes who had all but disappeared. They definitely made their presence felt this year with the carnage they inflicted on the bond market, both here in the U.S. and globally. We think they made bonds an interesting asset class once again, with sanity returning to the market pricing mechanism.

The most interesting market, which has numerous investment implications, is the foreign currency market. Beginning with the post-World War II Bretton Woods Agreement, U.S. hegemony was established and the dollar became the reserve currency of the world. This agreement was the beginning of globalization and free trade. As time marched on, the benefits of the system were numerous as it helped ensure cooperation amongst nations as trading partnerships developed. Formerly poor nations became wealthy as they were able to sell their exports to new markets. Importers benefited with the disinflationary impulse of cheaper goods. Free trade and globalization flourished as oil and other energy contracts were priced in U.S. dollars. After China’s entry into the World Trade Organization (WTO) in 2001, subsequent years saw a rise in globalization and a peak in global trade nearly two decades later. For the United States, the dollar’s reserve currency status gave it the ability to run much higher budget deficits, as those nations carrying a balance of payments surplus would invest those dollars in U.S. Treasuries, keeping interest rates lower than they otherwise would have been. Some of those dollars ended up in those surplus nation’s sovereign wealth funds and were subsequently recycled to the U.S. stock market. The demand for U.S. dollars also kept the currency well bid, and almost constantly overvalued relative to other currencies.

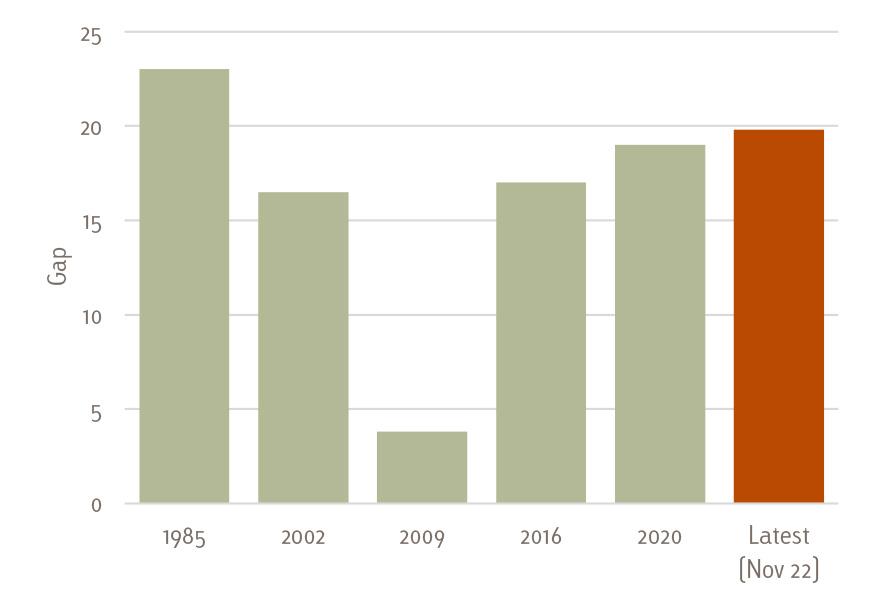

Over the past few years, there has been a realization that there are costs to the U.S. economy for globalization and the Bretton Woods Agreement. The hollowing out of American manufacturing and the middle class are two examples. Tensions between the U.S. and its chief rival and trade partner China have reached a critical point. The pandemic pointed out the flaws in over reliance on China for global supply chains. At various points, the U.S. has accused China of unfair trade practices, and China would like to establish itself as a global superpower and demand renminbi as payment for trade. The biggest blow to the current dollar as reserve currency system might be the recent weaponization of the dollar in geopolitics. Indeed, when Vladimir Putin invaded Ukraine in early 2022, the United States and Europe responded by seizing the dollar and euro denominated assets of Russian oligarchs. While well-intended and potentially justified, these actions could be sending a disturbing signal to the rest of the world that holds USD denominated assets. Governments such as Saudi Arabia might be wondering if they will receive the same treatment should they become the object of U.S. ire. Given the icy relationship between the two countries as of late, this is a distinct possibility. It is no wonder that Crown Prince Mohammed bin Salman has been meeting directly with President Xi Jinping of China to further their relationship and trade partnerships. There is speculation that the Saudis may sell their crude oil to China in exchange for renminbi. The meeting between the two leaders is especially notable since this was Xi’s first post-COVID meeting outside of China with a head of state. Other Middle Eastern and emerging market countries could find themselves in the same untenable position with the U.S. at some point and may move to politically align with others and diversify their reserves. We do not believe that the dollar will lose reserve status overnight, but given these political realities, we believe over the medium to long term, the USD will weaken relative to other currencies. From a valuation perspective, the dollar is about as overvalued as it gets when compared to historical peaks in the greenback.

As Louis Gave from Gavekal Research puts it, the U.S. stock market is probably the world’s most overvalued stock market, and it is denominated in the world’s most overvalued currency. Against that backdrop and the geopolitical winds discussed above, foreigners just might look to move their capital elsewhere.

Valuation Gap at Peaks of Goldman Sachs Real USD Trade-Weighted Index

Source: Goldman Sachs Global Investment Research

Source: Goldman Sachs Global Investment ResearchThe surprise move by the Bank of Japan on December 20 to loosen its yield curve control has the potential to reprice many asset classes globally throughout 2023. BOJ Governor Kuroda announced this after years of keeping the 10-year Japanese Government Bond (JGB) pegged at approximately 0.25% yield. With the Japanese yen (JPY) being the only relief valve available to the Japanese economy, investors and speculators mercilessly pounded the yen until it had depreciated 23.3% in USD terms, peak to trough in 2022. For its part, the BOJ was almost forced into this move as the interest rate differential between Japan and other developed markets became too much to bear. A one-way bet by speculators is never good for a nation’s currency and, in this case, it was impacting Japanese domestic inflation. In a surprise move, the BOJ put investors on notice that the one-way trade would no longer work, and that the biggest anchor in the global bond market (JGB) was finally unshackled. The investment implications for this could potentially be enormous as it could unleash a further sell-off in all bond markets as the Japanese are some of the world’s biggest savers and investors in foreign bond markets. With JGBs becoming more attractive and the currency strengthening (JPY appreciated 4.4% from the time of the announcement until the New York market close later that day), Japanese investors could take this opportunity to sell some of their foreign bond holdings and currencies while repatriating them back to yen denominated bonds. Additionally, Japanese equities could perform well with a nominal growth story underway in Japan and their relatively attractive valuation especially when compared to U.S. equities.

A weaker USD usually is a tailwind for the commodity complex. Coupling that with China’s abandonment of its Zero COVID policy, and a world still in short supply of energy, we think commodities could have a good year in 2023. As we outlined in last year’s outlook, the western world’s desire to produce more green energy also has positive implications for industrial metals.

Index Definitions

Goldman Sachs Real USD Trade-Weighted Index: A weighted average of the foreign exchange value of the U.S. dollar against the currencies of a broad group of major U.S. trading partners.

VIX Index: A real-time market index representing the market’s expectations for volatility over the coming 30 days.

NIKKEI Index: An index showing the average closing prices of 225 stocks on the Tokyo Stock Exchange.

Disclosures

Red Cedar Investment Management, LLC (“RCIM”) is an investment adviser registered under the Investment Advisers Act of 1940, , headquartered in Grand Rapids, MI. Registration as an investment adviser does not imply any level of skill or training. Any direct communication by RCIM with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of RCIM, please contact the United States Securities and Exchange Commission on their web site at http://www.adviserinfo.sec.gov/.

The information herein was obtained from various sources. RCIM does not guarantee the accuracy or completeness of information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. RCIM assumes no obligation to update this information, or to advise on further developments relating to it.