Insights

March 29, 2019

Investors’ search for investment income is not new. It has become a more important discussion after the 2008 financial crisis as yields plummeted during the age of Quantitative Easing by the Federal Reserve. Corporations were able to fund debt at historically low levels and some foreign governments issued debt with negative yields. Investors were left with hat in hand, searching for opportunities to enhance yields on portfolios without adding significant risk, or at least diversifying their risk appropriately. While some began taking a closer look at the preferred sector at this time, the team at Red Cedar had been managing the sector since 2002. Their experience in this unique sector has helped them to understand the nuances and opportunities that exist in a widely misunderstood asset class.

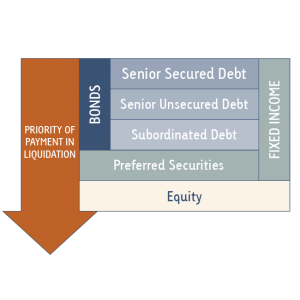

Preferred securities contain features of both bonds and stocks. They tend to trade and provide a benefit to portfolios similar to debt instruments, but many times exhibit features that would generally be associated with equity securities such as treatment of dividends. Their structure and treatment on a corporation’s balance sheet vary widely from issue to issue. Generally, the common denominator for preferred securities is where they fall in the capital structure of a company. In a bankruptcy and liquidation of a company, the holders of a preferred security would stand in line ahead of the equity owners but behind senior debt.

This “middle ground” often leads to misconceptions and inefficiencies for those not actively involved in the market. It is these inefficiencies that have led us to believe that the preferred market can provide opportunities for both attractive income and total return strategies that can be often overlooked.

Impact of Financial Reform

The financial services sector makes up a significant portion of the preferred market. While there are opportunities to mitigate some of this sector risk in an actively managed portfolio, it is still important to understand the nuances of this segment of the marketplace. Post the 2008 financial crisis and housing bubble, many changes have increased the regulatory environment around the banking and financial services sector. These regulations have been a headwind for equity investors while providing a larger cushion for debt and preferred securities investors. Balance sheets have been strengthened and risk controls improved. This has limited growth while strengthening a bank’s ability to survive another downturn in the economy.

The complexion of the preferred market has also been impacted as the regulatory framework for capitalizing banks has necessitated new preferred structures and the retiring of old ones that do not meet these new standards. The team at Red Cedar has been at the forefront of analyzing and investing in these new structures from day one of their introduction to the market. As the preferred market has evolved, the Red Cedar team has adapted to these changes, assessing the risks and potential rewards as new structures have replaced old ones.

Why Consider Preferreds?

Low Correlation to Traditional Asset Classes

Seeking opportunities to enhance the performance of an overall portfolio is nothing new in the asset management industry. One of the primary challenges of doing so is to find ways to improve performance while not taking outsized risk. Historically, many fixed income managers have utilized asset allocations to sectors, which seem to fit well into traditional bond portfolios by name but may introduce outsized risks relative to the alpha they add. High yield and emerging market exposure have been the allocation of choice for these managers over the past 20 years. Red Cedar believes that these sectors can, at times, provide positive risk-adjusted performance and may be appropriate on a case-by-case basis. However, we also believe that preferred securities offer an alternative way to introduce alpha into a fixed income portfolio while reducing correlations to other asset classes. Specifically, the correlations of high yield and emerging market debt are more closely correlated to both U.S. and global equities than preferred securities.

5-Year Correlation Matrix as of 12/31/2018

| Preferred | High Yield | S&P 500® | Aggregate | |

| Preferred | 1.000 | |||

| High Yield | 0.524 | 1.000 | ||

| S&P 500® | 0.291 | 0.583 | 1.000 | |

| Aggregate | 0.354 | -0.006 | -0.238 | 1.000 |

Source: B of A Merrill, S&P, Bloomberg

Yield Advantage to Traditional Securities

Over extended periods of time, yields tend to explain approximately 90% of fixed income market performance. The preferred securities sector provides an avenue to significantly enhance a portfolio’s overall yield while controlling risk, as evidenced by its correlation benefits. Compared to other segments of the broader fixed income universe, preferred securities stack up well on a yield comparison basis. Notably, preferred securities offer attractive yield while, in many cases, being issued by companies that have an investment grade rating at their senior debt level. While preferred securities do exhibit increased risk relative to their investment grade senior debt, it is distinct from traditional high yield debt.

Yield to Worst as of 12/31/2018

Sources: B of A Merrill, Bloomberg

Opportunities in an Inefficient Sector

Both the increasing complexity of the preferred market and the tendency for most of Wall Street’s research to overlook the sector can lead to significant inefficiencies. These inefficiencies may be difficult to exploit by some of the largest asset managers given the overall size of the preferred market relative to the global fixed income and equity markets. This space has also attracted a significant exchange-traded fund (ETF) presence. The ETFs’ attempt to replicate indices may drive them to purchase securities at unattractive levels. In many cases, we have noted securities priced with a negative yield to call. In an actively managed strategy, Red Cedar can take advantage of these opportunities. ETF portfolios must, at times, sell securities due to unexpected client liquidations. This forced liquidation provides Red Cedar an opportunity to purchase securities at attractive levels.

Other participants, such as retail investors and insurance companies, may have other unique circumstances driving their purchase and sell decision apart from maximizing total return. These circumstances can open doors to potential trades, which may provide attractive income and capital appreciation.

Red Cedar's Advantage

Experienced Team

The preferred market is complex and evolving. It will require an increased level of experience and analytical oversight to meet performance expectations. Continuous monitoring of the various preferred structures along with changing business dynamics create the need for experienced management of this sector. Combined, the Red Cedar team has over 100 years of professional asset management experience. The team has been involved in managing portfolios utilizing preferred securities as an asset class since 2002.

Investment Approach

The Red Cedar team uses a bottom-up fundamental approach in security selection and portfolio construction. The team draws upon its experience and expertise to assess both the credit profile of companies across the preferred universe and the covenant structure of each individual security. Other considerations in the investment process include the regulatory and operating environment as well as corporate governance.

The aforementioned factors help Red Cedar rank order the universe of potential investments. At that point, we apply relative value information to determine which securities offer an opportunity for excess return from either income or price appreciation. Red Cedar analyzes historical relationships versus other preferred securities and relative to other securities across the capital structure of the target issuer.

Once the team determines that a security and issuer offer a compelling risk adjusted opportunity, it is analyzed to ensure it fits within the overall framework of a portfolio. This process ensures that a security is appropriate and additive on a stand-alone basis and, also, within the overall framework of a client portfolio.

Size of Firm

Red Cedar Investment Management is able to take advantage of this market due to its size and experience within the fixed income and preferred markets. Many opportunities exist within fixed income markets and in the preferred market that may be attractive due to the size of the available securities. Red Cedar can take advantage of offerings that may not be meaningful to other large investors. As a boutique, Red Cedar can move quickly and efficiently across markets to take advantage of individual security opportunities. Our security selection process can add value and can be executed fluidly.

Red Cedar Investment Management believes that the preferred securities market offers substantial opportunities whether it is an allocation to an actively managed portfolio or utilized within a broader fixed income mandate. Our differentiated approach can provide enhanced yield, improved total return and lower correlations to traditional asset classes.